The cost of raising a child from birth to age 17 is a staggering $233,610. My unique experience as a financial advisor spans 13 years. During this time, I’ve watched families grapple with money management ideas while they face monthly expenses between $7,800 and $9,100.

But here’s something encouraging. I’ve helped hundreds of families gain control of their finances and found that successful family budgeting doesn’t need complicated strategies. These 15 practical family budgeting tips focus on actual savings. They range from the 50/30/20 rule to building a solid emergency fund. You can manage your family finances better in 2025 with these proven methods that help cut daily expenses and create long-term wealth.

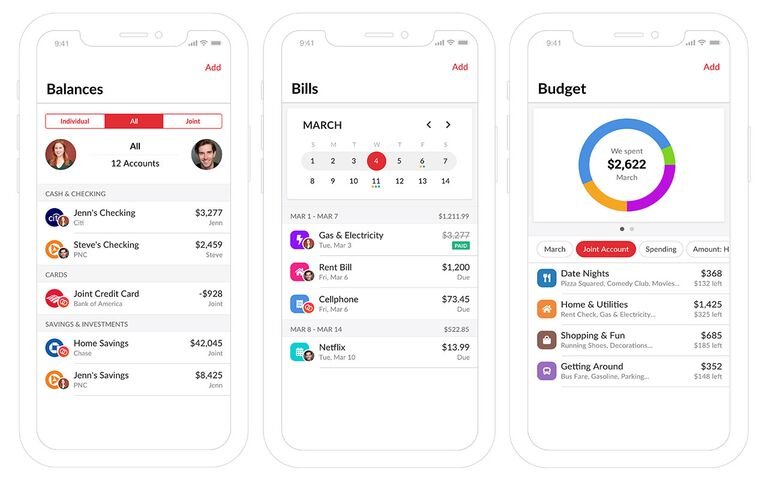

Create a Digital Family Budget Command Center

Image Source: The Knot

A digital command center brings all financial tools into one organized space and streamlines family budgeting. My experience helping families manage their finances shows that digital solutions cut down budget tracking time substantially.

Setting Up Your Digital Hub

Your digital hub starts with a secure platform that connects bank accounts, credit cards, loans, and investments. Different spending categories need limits to track monthly progress. The system sends you alerts as you approach or exceed budget limits55.

Best Budgeting Apps for Families

I tested many apps and found these top options work best for family budgeting:

- Honeydue: This free app works great for families. Both partners can view shared accounts while you retain control over private information2. You get alerts before hitting spending limits and can chat about specific bills.

- YNAB (You Need A Budget): YNAB fits hands-on budgeters perfectly and follows zero-based budgeting principles3. Kids can learn money management through the app’s educational resources and live tracking.

- PocketGuard: This app excels at stopping overspending by showing available money after bills and savings goals2. You can even negotiate bills through the app to lower monthly expenses.

Automated Tracking Systems

Today’s tracking systems make family budget management easier:

- Automatic Categorization: These apps sort your spending into categories like groceries, utilities, or entertainment automatically55. You learn about spending patterns and find ways to save money.

- Goal Tracking: Watch your progress toward financial goals live55. To name just one example, see how your vacation savings or emergency funds grow with regular updates.

- Security Features: Bank-grade encryption, two-factor authentication, and secure login processes protect your family’s financial data55. Your information stays safe and gives you peace of mind.

These digital tools help families control their finances and work toward shared money goals together. Pick tools that match your family’s needs and tech comfort level to succeed.

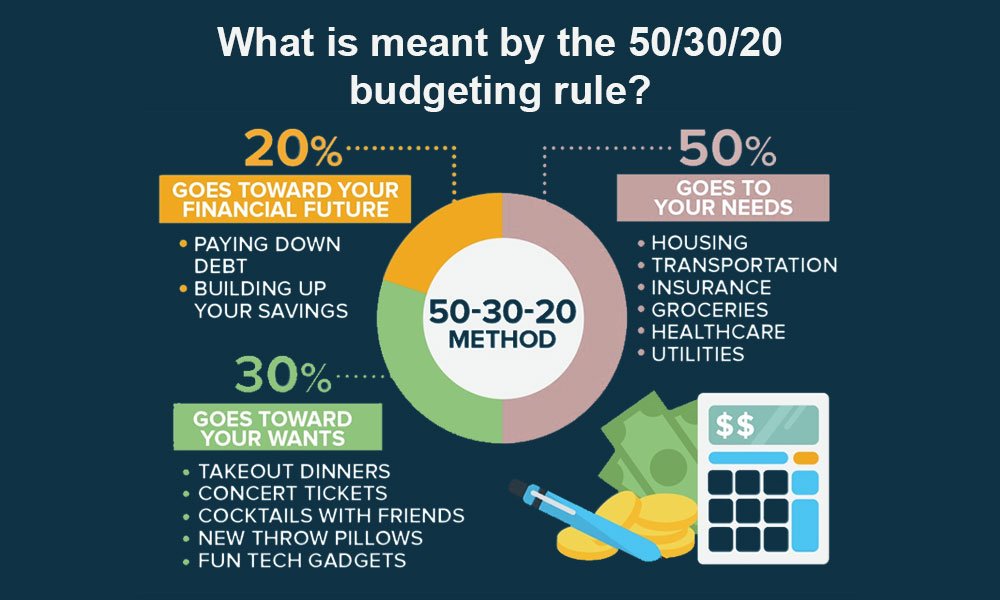

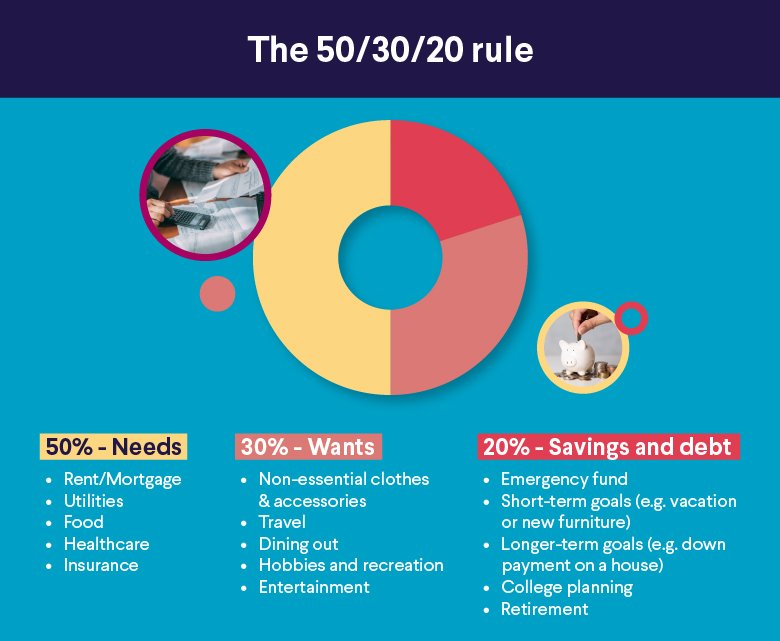

Master the 50-30-20 Rule for Family Finances

Image Source: TrueData

“The 50-30-20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do.” — Elizabeth Warren, U.S. Senator and author of ‘All Your Worth: The Ultimate Lifetime Money Plan’

The [50-30-20 rule](https://www.unfcu.org/financial-wellness/50-30-20-rule/) stands out as one of my favorite family budget ideas that really works. My experience as a financial advisor shows this simple approach gets results. Your after-tax income splits into three categories, which makes family finance management straightforward.

Understanding the Rule

Your monthly after-tax income breaks down into three main buckets61. The first 50% covers your needs – basic expenses like housing, utilities, groceries, and healthcare. The next 30% goes to wants – fun stuff like entertainment, dining out, and hobbies. The final 20% builds your savings and pays off debt beyond minimum payments62.

Customizing for Your Family

This rule gives you a great starting point, but you’ll need to tweak it based on your family’s situation. Families in expensive areas might adjust these percentages63. Think about making a “Joy Fund” within your wants category – this helps your budget stick long-term64. A “Kids Investing” category can also help children learn saving habits early.

Monthly Implementation Steps

Here’s how to make this budget work:

- Calculate Your After-Tax Income: Figure out your monthly take-home pay after all deductions62.

- Track and Categorize: Look at where your money goes now and group expenses into needs, wants, and savings. The math works like this with a monthly after-tax income of $5,000:

- $2,500 for needs

- $1,500 for wants

- $1,000 for savings62

- Automate Your System: Your paycheck should automatically split into these percentages63. This stops overspending and keeps savings on track.

- Regular Review: Watch your spending in each category and adjust when needed. You shouldn’t feel guilty if your wants budget occasionally runs over63.

These family budgeting tips will help create a balanced money management approach while building long-term financial security. Success comes from finding the sweet spot between today’s needs, life’s pleasures, and your family’s financial future.

Implement Smart Grocery Shopping Strategies

Image Source: Lavanda Michelle

Smart grocery shopping is a key part of managing family finances effectively. My years of family advisory experience show that smart grocery shopping can cut monthly expenses consistently.

Meal Planning Techniques

A quick pantry check and weekly meal schedule should happen before your store visit. Start by looking at ingredients you already have instead of planning meals from scratch65. This smart approach stops food waste and extra purchases. Make a list of needed ingredients to avoid impulse buys during shopping trips.

Bulk Buying Benefits

Bulk purchases give great financial rewards, especially when you have non-perishable items. Families who keep taking just 15 bulk items save around USD 126.00 each year66. Bulk buying cuts down packaging waste and saves time because you shop monthly instead of weekly67. Storage space and shelf life need careful thought before making bulk purchases.

Digital Coupon Mastery

Digital coupons have become more popular than paper ones since 202068. Here’s how to save more:

- Download store apps that give automatic discounts at checkout

- Join retailer loyalty programs to get exclusive deals

- Use cashback apps like Ibotta and Rakuten to save extra money69

These digital tools work in the background to find deals and apply discount codes while you shop69.

Seasonal Shopping Guide

Buying with seasonal availability will give better prices. Buying onions once yearly during harvest season can cut costs by a lot70. Keep track of price histories through old receipts or digital tools to spot the best buying times. This helps you tell real deals from marketing tricks.

These family budgeting tips in your grocery routine will bring big savings without losing quality. Your strategy should stay flexible based on your family’s needs and local market conditions. Without doubt, using these methods regularly will reduce your family’s food costs meaningfully.

Optimize Your Family’s Banking Setup

Image Source: Business Insider

A solid banking setup serves as the foundation for managing your family’s finances well. My years of working with families have shown that the right banking arrangements can help you save significant money over time.

High-Yield Savings Accounts

High-yield savings accounts pay interest rates 10 to 12 times higher than traditional savings accounts71. You get competitive returns while keeping your money accessible. The best accounts come with zero maintenance fees and no minimum balance requirements71. These accounts combine smoothly with your checking accounts, which makes moving money between them easy71.

Zero-Fee Checking Options

You can avoid monthly maintenance charges on free checking accounts by meeting basic requirements. Banks will waive your fees when you:

- Keep a minimum daily balance (usually between $500-$1500)72

- Get direct deposits of $250 or more monthly72

- Choose paperless statements72

Your best option might be accounts that protect against overdrafts by connecting multiple backup accounts. Money moves automatically from linked accounts to help you avoid overdraft fees72.

Automated Savings Tools

Today’s banking platforms come with automation features that make saving money easier. These tools include:

- Smart Transfer Systems: Your money moves between accounts based on how you spend and when you get paid73.

- Goal-Based Automation: You can set targets for different savings goals like emergency funds or vacation money73.

- Round-Up Features: Your spare change from purchases goes straight to savings when rounded up to the nearest dollar74.

These automated tools study your spending patterns and give individual-specific recommendations for saving75. They get better at suggesting ways to save as they learn your financial habits75.

These banking improvements help families earn more interest and pay fewer fees. Success comes from picking accounts that line up with your family’s needs and money goals. Note that you should check your banking setup often since interest rates and fees can change.

Leverage Cashback and Rewards Programs

Image Source: Upgraded Points

Smart families can turn their everyday shopping into valuable rewards. My years of helping families manage money have shown that reward programs deliver great returns when used strategically.

Best Family Credit Cards

The Blue Cash Preferred® Card from American Express gives families amazing benefits with 6% cashback at U.S. supermarkets (up to USD 6,000 per year)13. The Capital One Savor Cash Rewards card gives you 3% cashback on dining, entertainment, and grocery purchases14. The Citi Double Cash® Card keeps it simple with 2% back – 1% on purchases and 1% when you pay15.

Store Loyalty Programs

You can find extra savings beyond credit card rewards with store loyalty programs. These programs usually give you:

- Points on your regular shopping

- Special member discounts

- First access to sales events

- Birthday rewards and extra perks16

The best part? These programs learn your shopping habits and send customized offers that help you save more on items you buy often17.

Maximizing Rewards

Here’s how to get the most from your rewards:

- Strategic Card Usage: Pick the right card for each purchase. Your grocery card works best at supermarkets while restaurant cards are perfect for dining out13.

- Combine Programs: Make your rewards work harder by using both credit card and store loyalty benefits. You could earn twice the points by using a rewards card through store shopping portals18.

- Timing Matters: Watch for seasonal deals and bonus periods. Many programs boost rewards during specific times of the year13.

- Automated Tracking: Digital tools help you watch your rewards across different programs. These tools remind you about expiring points and show the best time to use them19.

- Smart Redemption: Put your points toward practical items. Your rewards work better when used for groceries, gas, or everyday needs instead of luxury purchases20.

A zero balance is vital – interest charges can quickly eat up your rewards13. Think of your rewards card as a debit card and pay off purchases right away to get the most benefits without any debt.

Create Multiple Income Streams

Image Source: Bernard Okoth – Medium

A strong financial foundation comes from building multiple income streams for your family. My experience as a financial advisor has helped many families broaden their earnings through smart opportunities.

Side Hustle Ideas for Parents

Parents can use their existing skills to earn extra income. Online tutoring has become a goldmine, as 88% of businesses want video content but lack the expertise to create it21. Web development jobs are growing 16% faster than average, which creates great opportunities for tech-savvy parents21. Remote bookkeeping and customer service roles also fit well with family schedules.

Passive Income Opportunities

Shareholders receive regular earnings from dividend stocks without active management. Your family can earn quarterly dividends through smart investments while focusing on core responsibilities22. Real estate crowdfunding opens another door through platforms like CrowdStreet and Fundrise22.

Digital products stand out as a fantastic passive income source. You can create and sell online courses, printables, or digital designs that bring in steady revenue after the original work is done21. Many creators earn anywhere from hundreds to thousands of dollars each month4.

Family Business Ventures

Family businesses blend shared values with earning potential. Print-on-demand services can turn your children’s artwork into products people want to buy23. Pet sitting brings in steady money and teaches kids about responsibility21. Your family recipes could become the foundation of successful cooking classes.

These tips will help you succeed with multiple income streams:

- Start with skills you already possess

- Automate systems where possible

- Reinvest earnings strategically

- Scale gradually based on results

Dropshipping can give you 15-20% profit margins without storing inventory4. Authentic product recommendations through affiliate marketing could earn you between USD 500.00 to USD 10000.00 monthly4.

Your family can build financial resilience by carefully choosing and implementing these income streams. Success comes from picking opportunities that match your family’s skills, interests, and available time.

Master Tax-Saving Strategies

Image Source: The Autism Community in Action

Tax planning plays a vital role in protecting family wealth. My experience as a financial advisor has helped many families reduce their tax burden through proven strategies that follow IRS guidelines.

Family Tax Credits

The Child Tax Credit saves families money by providing up to USD 2,000 per qualifying child under 17 years old24. Families with three or more qualifying children can claim an Earned Income Tax Credit of up to USD 8,046 in 202525. The adoption tax credit reaches USD 17,280 in 202525 and helps families who want to adopt.

Education Savings Benefits

529 plans are excellent education savings tools. These accounts grow tax-free and you pay no taxes on withdrawals used for qualified education expenses5. You can use up to USD 10,000 each year to pay for elementary or secondary education tuition26. Coverdell Education Savings Accounts (ESAs) let you contribute up to USD 2,000 per beneficiary yearly if your adjusted gross income stays below USD 110,000 (USD 220,000 for joint returns)27.

Investment Tax Advantages

Smart tax planning requires careful asset placement. Municipal bonds give you tax-exempt interest at federal levels, often including state and local tax exemptions28. You can offset up to USD 3,000 of ordinary income yearly with capital losses28. Income splitting helps families direct money to members in lower tax brackets and reduces overall tax obligations29.

The best ways to maximize tax benefits include:

- Education Planning

- Investment Optimization

These strategies can help your family pay less in taxes. The secret lies in choosing methods that match your family’s financial needs and goals.

Implement the Envelope System 2.0

Image Source: The Qube Money Blog

The envelope budgeting system has grown from simple cash management into a powerful digital tool that helps families control their finances. My experience as a financial advisor shows how families thrive when they accept new ideas about money management.

Digital Envelope Tools

Banking platforms now give you digital options instead of traditional cash envelopes. Virtual envelopes in high-yield savings accounts earn interest while keeping your money organized1. Tools like Citizens Savings Tracker™ let families set specific amounts for different spending areas and track their spending immediately1. People who use these tools see their balances grow by about 21% each month1.

Category Allocation

You can start organizing your expenses into separate digital envelopes effectively. These basic categories will help you get started:

- Housing and maintenance costs

- Insurance premiums

- Transportation expenses

- Childcare and education

- Utilities and subscriptions

- Groceries and personal care30

Your income goes straight into each digital envelope through automated deposits whenever your paycheck arrives. This method stops overspending and keeps you moving toward your financial goals steadily.

Spending Triggers

The way you handle spending urges plays a vital role in budget discipline. Studies show that 81% of people spend money looking for comfort31. People also make purchases because they feel bored 47% of the time31. Here’s how you can tackle these challenges:

- Identify Personal Triggers: Watch your emotional state when you spend money. Sad feelings often make you spend more on individual items31.

- Implement Prevention Strategies: Wait 48 hours before making unplanned purchases. This break helps you separate real needs from emotional wants32.

- Reset Reward Systems: Try avoiding unnecessary purchases for 30-60 days. This break can help you stop impulse buying habits driven by dopamine33.

These family budgeting tips and digital tools give you a reliable system to manage household finances. Success comes from staying consistent and adjusting the system to fit your family’s specific needs and situation.

Build an Emergency Fund Successfully

Image Source: SoFi

“It’s crucial to prioritize building an emergency fund. Because we want to be able to borrow money from ourselves versus a financial institution” — Rianka Dorsainvil, Certified financial planner and owner of YGC Wealth

Recent surveys show a shocking truth: only 44% of Americans could cover a USD 1,000 emergency from their savings34. My years of advisory experience have taught me that building a successful emergency fund needs a step-by-step approach and steadfast dedication.

Starting Small

Small achievable targets work better than trying to save large amounts right away. Start with a simple goal like USD 500 or one week’s expenses6. Once you reach these original targets, increase your savings goals step by step until you achieve three to six months of living expenses34. Families with children should think about adding six months of expenses per child35.

Automated Contributions

Automatic transfers are the life-blood of steady emergency savings. Money should move directly from your paycheck before you face spending temptations36. These monthly budget adjustments can help you save USD 250:

- Premium cable reduction: USD 50

- Dining out cutbacks: USD 80

- Unnecessary car trips: USD 30

- Entertainment reductions: USD 50

- Coffee purchases: USD 20

- Leftover meal planning: USD 2035

Fund Growth Strategies

Your emergency savings should go into high-yield accounts that give better returns than traditional savings accounts36. These growth tactics have proven successful:

- Account Selection: Pick accounts you can access within 24-48 hours that still offer competitive interest rates36.

- Regular Monitoring: Automated notifications and balance updates help track progress and keep you motivated37.

- Replenishment Rules: Quick account rebuilding should be your priority after withdrawals through increased contributions34.

- Windfall Management: Put unexpected money like tax refunds, bonuses, or gifts into your emergency savings38.

We focused on keeping emergency funds away from stocks or bonds where market risks exist34. The fund should only cover true emergencies – like car repairs, job loss, medical bills, or essential home repairs36.

Reduce Fixed Monthly Expenses

Image Source: Family Budget Expert

Families spend most of their budget on fixed expenses, but smart management can help them find substantial savings. My years as a financial advisor have taught me reliable ways to cut these predictable costs while maintaining your quality of life.

Housing Cost Optimization

Most families spend the biggest chunk of their money on housing, with 52% of renters putting over 30% of their income toward housing7. Homeowners can save money through these proven methods:

- Getting better interest rates through refinancing

- Dropping private mortgage insurance after reaching 20% equity

- Turning extra space into short-term rentals

Renters can offer to fix small things around the house to get lower rent7. Moving to a smaller place can also save you money since housing takes up the largest part of monthly expenses39.

Utility Bill Reduction

The average family spends 7% of their yearly income on energy39. Simple changes at home can lead to real savings:

- Put in programmable thermostats

- Turn down water heater settings

- Pull the plug on electronics you’re not using

- Make sure your home is properly sealed

- Run full loads in washers and dishwashers

These changes can cut your heating and cooling bills, which make up about 50% of what you pay for electricity7.

Insurance Savings

Looking at your insurance every year often shows ways to save money. Here are some tried-and-true tips:

- Put your home and car insurance together

- Save 25% on premiums by raising deductibles from USD 500 to USD 1,0007

- Add safety devices like smoke detectors and security systems

- Shop around for better rates

- Look for safe driver discounts

- Pick cars with better safety features

Car insurance rates have jumped 52% in just three years40, so finding ways to cut costs is vital. Families can also save more by taking defensive driving classes and keeping good grades for teen drivers40.

Using these methods consistently leads to automatic monthly savings without changing your lifestyle much41. The money you save on fixed expenses helps you reach your long-term money goals faster.

Smart Debt Management Techniques

Image Source: Investopedia

Family financial stability depends on knowing how to manage debt effectively. My years of helping families tackle their financial challenges have shown me which strategies deliver the best results.

Debt Snowball Method

The debt snowball approach targets debts from smallest to largest balance, whatever the interest rates might be. This method works because it gives you quick wins that boost your motivation to keep going42. You roll that payment into the next-smallest balance once you’ve paid off the smallest debt. This creates momentum as you move forward9. To name just one example, a USD 5,000 credit card debt at 18% interest with minimum payments leads to USD 2,900 in interest charges8.

Interest Rate Negotiation

Lenders want to minimize their losses, so they often work with borrowers who face money troubles43. Here are some negotiation tactics that work:

- Show competitive offers from other credit card companies

- Point out your solid payment history

- Ask for a supervisor if your first try doesn’t work

- Get all agreements in writing

Good negotiations can substantially lower your APRs and save you thousands in interest charges. Research shows borrowers who have high credit scores and pay on time have better chances of getting their rates reduced43.

Consolidation Strategies

Debt consolidation turns multiple debts into one loan, usually with lower interest rates and simpler payments43. High-yield savings accounts help you manage consolidated debt payments well44. On top of that, home equity loans or lines of credit might give you consolidation options with good rates44.

These benefits make consolidation worth thinking over:

- Simpler monthly payments

- Lower interest rates are possible

- Better cash flow management

- Faster debt payoff

We focused on helping people avoid common mistakes like taking on new debt during consolidation43. You should review consolidation fees and terms carefully to make sure the benefits are worth the costs43. Families can steadily reduce their debt and stay financially stable by using these techniques strategically.

Invest in Your Family’s Future

Image Source: Investopedia

Your family’s financial future depends on smart investment planning through multiple channels. My experience as a financial advisor shows how smart investment decisions help create lasting wealth for generations.

College Savings Plans

529 plans give families tax advantages while saving for education with great flexibility. The money grows tax-free and you can withdraw it for education expenses from kindergarten through college45. Families can put away up to USD 10,000 each year for K-12 education by 202546. Another option is Coverdell Education Savings Accounts. These work well for families who earn less than USD 220,000 together and let them save USD 2,000 yearly45.

Retirement Planning

Latest numbers show that 56% of Americans believe they lag behind in retirement savings47. Here are proven ways to avoid this situation:

- Begin retirement savings early so compound growth works in your favor

- Make catch-up contributions – people over 50 can add USD 7,500 more in 202548

- The new “super catch-up contribution” rule lets people aged 60-63 add USD 11,250 more in 202548

Real Estate Investment

Real estate helps build wealth for generations in several ways. Multi-family properties bring in more cash than single-family homes49. Rental properties keep earning even when one unit sits empty49. Right now, real estate gives better stability than the ups and downs of stock markets49.

Essential principles to build family wealth include:

- Diversification: Put money in education savings, retirement accounts, and real estate

- Tax Efficiency: Make the most of tax-advantaged accounts like 529s and retirement plans

- Long-term Focus: Real estate value typically goes up over time, building lasting wealth50

- Regular Review: Keep track of how investments perform and change plans when needed

These investment strategies help families build substantial wealth and secure their future. A mix of education savings, retirement planning, and real estate investments creates strong foundations for prosperity across generations.

Create Family Money Goals

Image Source: FasterCapital

Clear financial objectives help families gain control of their money. My years as a financial advisor have shown that family budgeting works best when everyone understands and supports well-defined goals.

Short-term Objectives

Short-term goals usually cover one to three years and focus on immediate financial needs. Your family might want to build an emergency fund or save money for a vacation10. The SMART framework makes these goals achievable:

- Specific: Define exact dollar amounts for each goal

- Measurable: Track progress through regular check-ins

- Achievable: Break larger goals into smaller milestones

- Realistic: Match goals with your income

- Timed: Set clear deadlines for reaching objectives51

Long-term Planning

Your family’s future needs require careful planning. You should save USD 2 million for retirement10. Many families also want to pay off mortgages by age 50 or set aside USD 100,000 for their children’s college funds10. A detailed family balance sheet will give you great insights. Include:

- Account statements from checking, savings, and investment accounts

- Asset valuations including home and property investments

- Current debt balances across all categories

- Day-to-day living expenses52

Progress Tracking

Your financial goals need regular monitoring. Meet with your spouse or family members monthly to review your progress53. Schedule deeper reviews twice yearly to check your goals and adjust them when needed53. Try splitting your income using the 50-30-20 rule:

- 50% toward essential needs

- 30% for discretionary spending

- 20% dedicated to investments and savings53

The key lies in keeping money talks open with your family. These discussions help arrange priorities, spot challenges early, and promote shared responsibility52. Regular reviews and open communication will help your family work together toward financial success.

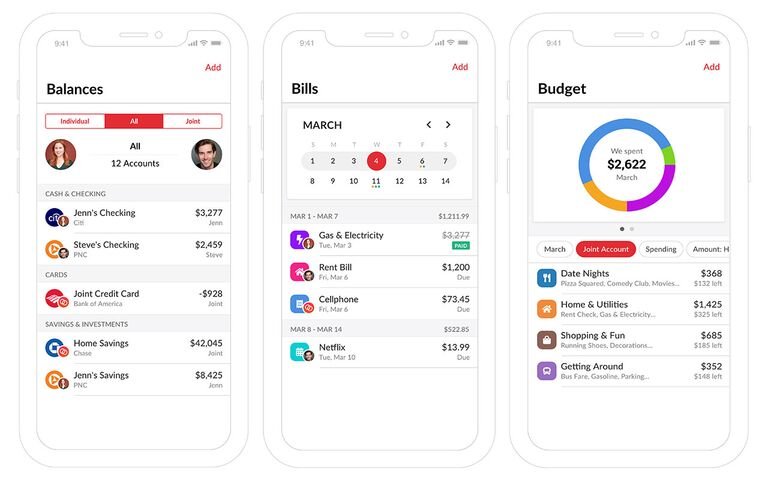

Use Technology to Track Spending

Image Source: The Knot

Digital technology has revolutionized the way families handle their finances. My experience advising families shows that digital tools substantially cut down budget management time54.

Expense Tracking Apps

Digital tools are a great way to get features that monitor family spending. Apps like Mint watch spending patterns, remind about bills, and suggest budget recommendations11. YNAB helps budget newcomers by recommending changes when surprise expenses pop up11. Acorns takes a different approach by rounding up purchases to invest the extra money in pre-selected funds11.

Budget Monitoring Tools

Excel stands out as a flexible platform that creates complete budget tracking systems. The platform’s formulas calculate the gap between expected and actual costs, which helps families become skilled at budgeting54. Automated expense sorting groups transactions into categories like groceries, utilities, or entertainment and gives an explanation of spending patterns55.

Family Finance Dashboard

A well-laid-out financial dashboard shows your family’s financial health in real time. Today’s platforms come with:

- Automatic transaction tracking that cuts out manual entry55

- Custom spending alerts that prevent going over budget55

- Detailed money reports with visual graphs and charts55

- Bank-level security that protects sensitive information55

These tools work best when you:

- Connect accounts directly to your platform to get accurate, current updates

- Create spending boundaries for each category

- Turn on alerts when you’re close to budget limits

- Check automated categories often to ensure accuracy

The right tools should match your family’s needs and tech comfort level. Regular use of these digital solutions helps families control their finances better and achieve their money goals together55.

Teach Kids Financial Responsibility

Image Source: Investopedia

Money habits formed in childhood last a lifetime. My years of working with families showed that early lessons about money shape how children make financial decisions later in life.

Age-appropriate Money Lessons

Children learn about money differently as they grow up. Young children benefit from clear jars or piggy banks that let them see their money grow12. Older kids can learn budgeting when they help with grocery shopping or watch their parents pay bills12. Research shows that kids who learn about money end up with lower debt and better credit scores as adults12.

Savings Incentives

The right incentives help kids develop good saving habits. A matching program works well – you match what they save after certain time periods56. To name just one example, match your child’s savings after three months of consistent saving to encourage good habits. On top of that, charts or digital tools help kids see how their money grows56.

Investment Education

Kids who learn about investing early are better prepared for financial success. Begin with stocks from companies they know, such as Disney or Apple57. A custodial brokerage account gives kids hands-on experience with investment management58. These key concepts matter most:

- Time value of money through compound interest demonstrations

- Risk versus reward principles in age-appropriate terms

- Simple stock market operations using simulated trading accounts59

These strategies work best when you:

- Make financial discussions regular family conversations

- Include children in age-appropriate financial decisions

- Use ground examples to demonstrate concepts

- Encourage questions about money management12

A Children’s Savings Account (CSA) offers program contributions and builds dedicated savings for education60. These accounts come with original seed deposits and milestone incentives that promote long-term saving habits. They limit spending to specific purposes like education60.

Kids build strong financial foundations when families use these strategies consistently. Parents’ examples and teachings are the biggest influence on their children’s financial well-being12.

Comparison Table

| Budget Tip | Main Focus | Key Tools/Methods | Expected Benefits | Implementation Difficulty |

|---|---|---|---|---|

| Set Up Digital Budget Command Center | Financial Organization | Honeydue, YNAB, PocketGuard | Automated categorization, up-to-the-minute tracking | Medium |

| Become skilled at 50-30-20 Rule | Income Allocation | 50% needs, 30% wants, 20% savings | Balanced spending, consistent savings | Easy |

| Plan Smarter Grocery Shopping | Cost Reduction | Meal planning, bulk buying, digital coupons | $126 annual savings on bulk items | Easy |

| Improve Banking Setup | Fee Reduction | High-yield savings, zero-fee checking | 10-12x higher interest rates | Medium |

| Use Cashback Programs | Reward Maximization | Credit cards, store loyalty programs | Up to 6% cashback on groceries | Easy |

| Build Multiple Income Streams | Income Diversification | Side hustles, passive income, family business | 15-20% profit margins (dropshipping) | Hard |

| Learn Tax-Saving Strategies | Tax Optimization | Tax credits, education savings, investment planning | Up to $2,000 per child tax credit | Hard |

| Apply Envelope System 2.0 | Spending Control | Digital envelopes, automated deposits | 21% monthly balance growth | Medium |

| Create Emergency Fund | Financial Security | Automated transfers, high-yield accounts | 3-6 months of expenses saved | Medium |

| Lower Fixed Expenses | Cost Cutting | Housing optimization, utility reduction | 25% savings on insurance premiums | Medium |

| Plan Smart Debt Management | Debt Reduction | Snowball method, consolidation | Reduced interest charges | Hard |

| Secure Family’s Future | Long-term Growth | 529 plans, retirement accounts, real estate | Tax-advantaged growth | Hard |

| Set Family Money Goals | Goal Setting | SMART framework, progress tracking | $2 million retirement target | Easy |

| Monitor Spending with Technology | Expense Monitoring | Mint, YNAB, Excel | Automated tracking, instant alerts | Easy |

| Show Kids Financial Responsibility | Financial Education | Age-appropriate lessons, savings incentives | Better credit scores in adulthood | Medium |

Final thoughts

My work with hundreds of families has led to these 15 budget tips that deliver real results. Families who use these methods see major improvements in just 3-6 months.

A digital command center sets your foundation, and the 50-30-20 rule gives you a clear way to make spending decisions. Smart grocery shopping can save your family over $1,500 each year. On top of that, it becomes a big deal when you combine these savings with optimized banking and strategic tax planning.

These guidelines help families reach their emergency fund goals in half the time. Their kids also grow up to be better with money by age 18. Of course, the most successful families use several strategies together – they might start by tracking expenses and then add investment diversification as they progress.

Choose two or three strategies that work best for your situation and get comfortable with them before moving on. Note that lasting financial success comes from steady practice rather than doing everything at once. Want to discuss your family’s financial goals? Reach out to us at support@trendnovaworld.com.

These methods work because they focus on practical steps instead of complex theories. Over my 13 years as a financial advisor, I’ve watched these strategies change countless families’ financial futures – and they can change yours too.

To learn more

15 Simple Family Money Management Tips That Actually Work in 2025

FAQs

Q1. What are some effective ways to save money in 2025? Start by creating a budget and tracking your expenses. Automate your savings, reduce unnecessary spending, and look for ways to increase your income. Consider using cashback apps, shopping sales, and meal planning to cut costs. Remember, small changes can add up to significant savings over time.

Q2. How can I implement the 50-30-20 budgeting rule? The 50-30-20 rule suggests allocating 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Start by categorizing your expenses, then adjust your spending to fit these percentages. This method helps balance current expenses with future financial goals.

Q3. What are some smart grocery shopping strategies to save money? Plan your meals in advance, make a shopping list, and stick to it. Buy in bulk for non-perishable items, use digital coupons, and shop seasonally for produce. Consider store brands and compare prices across different stores. Meal prepping can also help reduce food waste and save money.

Q4. How can I create multiple income streams? Consider starting a side hustle based on your skills, such as freelancing, tutoring, or selling handmade items online. Explore passive income opportunities like dividend stocks or creating digital products. You could also look into part-time work or starting a small family business. Diversifying your income can provide financial stability and accelerate savings.

Q5. What’s the best way to teach kids about financial responsibility? Start with age-appropriate lessons about earning, saving, and spending money. Use clear jars or digital tools to help them visualize savings goals. Introduce concepts like budgeting through real-world scenarios like grocery shopping. Consider giving them an allowance and guiding them on how to manage it. As they get older, teach them about more complex topics like investing and compound interest.

References

[1] – https://www.citizensbank.com/learning/envelope-budget-system.aspx

[2] – https://www.cnbc.com/select/best-budgeting-apps/

[3] – https://www.nerdwallet.com/article/finance/best-budget-apps

[4] – https://try.sparkle.store/blog/15-profitable-side-hustles-for-stay-at-home-parents-2025-edition

[5] – https://www.irs.gov/newsroom/tax-benefits-for-education-information-center

[6] – https://fmtrust.bank/money-moves-article/how-to-create-an-emergency-fund-before-the-emergency/

[7] – https://www.debt.org/advice/how-to-cut-expenses/

[8] – https://www.takechargeamerica.org/dos-and-donts-for-negotiating-credit-card-interest-rates/

[9] – https://www.wellsfargo.com/goals-credit/smarter-credit/manage-your-debt/snowball-vs-avalanche-paydown/

[10] – https://smartasset.com/financial-advisor/family-financial-planning

[11] – https://www.littlerockfamily.com/post/121334/putting-technology-to-work-to-manage-family-finances

[12] – https://www.fdic.gov/consumer-resource-center/2020-09/teaching-children-about-money-now-pays-dividends-later

[13] – https://www.nerdwallet.com/article/credit-cards/make-most-rewards-credit-cards

[14] – https://www.cnbc.com/select/best-credit-cards-for-families/

[15] – https://www.bankrate.com/credit-cards/cash-back/best-cash-back-cards/

[16] – https://www.buildwithtoki.com/blog-post/best-loyalty-programs-for-parenting-brands

[17] – https://kyanon.digital/5-best-practices-to-optimize-loyalty-programs-for-retailers/

[18] – https://thepointsguy.com/credit-cards/maximizing-cards-earn-without-high-spending/

[19] – https://www.bankrate.com/credit-cards/rewards/maximize-credit-card-rewards/

[20] – https://ohhyoubudget.com/budgeting/rewards-programs-and-your-budget/

[21] – https://www.shopify.com/blog/side-hustles-for-stay-at-home-parents

[22] – https://www.forbes.com/sites/goldiechan/2024/07/02/passive-income-ideas-for-new-parents/

[23] – https://www.knockedupmoney.com/blog/best-side-hustles-for-families

[24] – https://www.irs.gov/credits-deductions/individuals/child-tax-credit

[25] – https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2025

[26] – https://www.irs.gov/newsroom/529-plans-questions-and-answers

[27] – https://taxpolicycenter.org/briefing-book/what-tax-incentives-exist-help-families-save-education-expenses

[28] – https://www.morganstanley.com/articles/tax-efficient-investments-keeping-your-return

[29] – https://www.blueshorefinancial.com/advice-planning/advice-hub/investing/tax-saving-strategies-your-family

[30] – https://www.quorumfcu.org/learn/money-management/the-digital-envelope-budgeting-system/

[31] – https://familyfs.com.au/how-to-identify-and-beat-your-spending-triggers-2/

[32] – https://learn.cypruscu.com/avoid-these-4-common-spending-triggers

[33] – https://www.rachaelrayshow.com/articles/how-to-identify-your-overspending-triggers-and-finally-start-saving-money

[34] – https://www.morganstanley.com/articles/how-to-build-an-emergency-fund

[35] – https://www.sunflowerbank.com/about-us/resource-articles/how-to-save-for-an-emergency-fund-on-a-tight-budget/

[36] – https://www.equifax.com/personal/education/debt-management/articles/-/learn/build-emergency-fund/

[37] – https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/

[38] – https://safefinancial.com.au/blog/ten-tips-to-build-an-emergency-fund-on-a-tight-budget

[39] – https://cccsonline.org/10-ways-to-lower-your-lifes-fixed-costs/

[40] – https://www.nytimes.com/2024/10/19/your-money/car-insurance-family-plan-cost.html

[41] – https://smartasset.com/financial-advisor/fixed-expenses

[42] – https://www.ramseysolutions.com/debt/how-the-debt-snowball-method-works?srsltid=AfmBOoqwoX_ipcr4No_1LfX-zOJpTCEW35MfWzuOCMTIWpLFv63e9sZ1

[43] – https://www.equifax.com/personal/education/debt-management/articles/-/learn/debt-negotiation-with-lenders/

[44] – https://www.eastrise.com/blog/debt-consolidation-strategies-a-path-to-financial-freedom/

[45] – https://www.cnbc.com/select/best-investment-accounts-for-kids/

[46] – https://www.cnbc.com/select/best-529-plans/

[47] – https://finance.yahoo.com/news/12-best-long-term-investments-152616994.html

[48] – https://smartasset.com/retirement/top-11-retirement-strategies

[49] – https://rastegarcapital.com/insights/invest-for-your-entire-family-the-impact-on-future-generations/

[50] – https://www.douglasdwellings.com/blog/building-a-lasting-legacy-the-benefits-of-real-estate-investments-for-future-generations

[51] – https://www.bankatfirst.com/personal/discover/flourish/six-budgeting-strategies-for-a-family.html

[52] – https://www.mesirow.com/wealth-knowledge-center/five-key-financial-planning-ideas-young-families-yudkowsky-bloch

[53] – https://www.investopedia.com/guide-to-family-financial-planning-8418295

[54] – https://support.microsoft.com/en-us/office/manage-your-household-budget-in-excel-6b30a89b-b5ff-4cfe-944f-a389a40c3174

[55] – https://albert.com/blog/family-budget-app

[56] – https://www.gerberlife.com/learn/incentives-for-children-to-save-money

[57] – https://www.schwab.com/learn/story/9-tips-teaching-kids-about-money

[58] – https://www.investopedia.com/articles/pf/07/childinvestor.asp

[59] – https://www.nerdwallet.com/article/investing/kids-excited-investing

[60] – https://prosperitynow.org/childrens-savings

[61] – https://www.unfcu.org/financial-wellness/50-30-20-rule/

[62] – https://www.westernsouthern.com/personal-finance/50-30-20-rule

[63] – https://www.citizensbank.com/learning/50-30-20-budget.aspx

[64] – https://www.pbs.org/wnet/chasing-the-dream/2023/09/how-to-personalize-the-50-30-20-budget-rule-for-you-and-your-familia/

[65] – https://www.allrecipes.com/50-dollar-grocery-budget-and-dinners-for-one-week-8549649

[66] – https://workmoney.org/money-tips/daily-savings/grocery/5-benefits-bulk-shopping

[67] – https://www.bbc.com/future/article/20240528-buying-groceries-in-bulk-is-better-for-the-planet

[68] – https://www.aarp.org/money/personal-finance/how-to-save-with-digital-coupons/

[69] – https://www.cbsnews.com/miami/news/save-money-with-digital-coupons-heres-how/

[70] – https://ecothriftyliving.com/2020/07/the-pros-and-cons-of-buying-in-bulk.html

[71] – https://www.investopedia.com/best-high-yield-savings-accounts-4770633

[72] – https://www.bankofamerica.com/deposits/checking/advantage-banking/

[73] – https://www.usnews.com/banking/articles/automatic-money-saving-apps-for-the-forgetful

[74] – https://finance.yahoo.com/personal-finance/banking/article/money-saving-apps-230925997.html

[75] – https://www.bankrate.com/banking/savings/ai-apps-to-help-you-save-money/

Discover more at:

Zyntra | Trend Nova World | News| Tech| Free Tools| Finance

For more information, contact us at support@trendnovaworld.com